TLDR:

- Through strong but false narratives, MicroStrategy shares are trading at a large premium to net assets. From this premium, a “Bitcoin yield” is extracted through ATM offerings and convertible bond issuance. The premium provides an arbitrage to the company, which now captures it in the largest ATM offering in human history.

- New investors are still bidding on shares at a premium because of the high “Bitcoin yield” marketed by the company. Unbeknownst to most of them, the investors contribute said yield. They are the yield. This Ponzi element of the company can occur while the circular reasoning persists.

- When the pool of new investors shrinks, the Bitcoin yield as a percentage of owned Bitcoin must decline towards zero, causing heavy losses for investors entering late into the scheme or at high NAV multiples.

My interest in the story of MicroStrategy started out tangential at first — it was just one of many unconventional outcomes born out of the rising Bitcoin phenomenon. The publicly traded company, although first in the world to pursue a Bitcoin accumulation strategy, flew under the radar of most conventional investors, and it was only after the long Bitcoin winter of 2022 and early 2023 that both old and new narratives from the company and its de facto leader, Michael Saylor, broke through the thawing ice and began to spread among a bewildered audience. 2024 catapulted MicroStrategy to new sensational heights, and I soon realized I was witnessing financial history in the making. The general enthusiasm was unparalleled; sons went “all in” with the savings of their parents while old investors bought new houses from quick gains on leveraged positions. Any public display of hesitation to the many optimistic narratives energizing investment circles was met with scorn or silence. When logical arguments against the company’s ever higher valuation to net assets were put forward, they were answered by vague appeals to unofficial thought leaders or to a vision of a utopian future. On the verge of letting this one be altogether and mentally filing it as just another financial bubble soon to pop, I finally made the decision to work on this report as a veiled but growing Ponzi-scheme element of MicroStrategy’s business became ever clearer. So, having delved deep into the facts and fiction underlying common investor assumptions, it is now my firm belief that what is going on with MicroStrategy will end in disaster for most investors, should affairs not radically alter. It is a play of five parts, presented chronologically to the reader.

Emil Sandstedt, 2024–12–06

MicroStrategy’s early history is laid to rest behind a thin curtain, mostly undisturbed by the hands of modern investors. It is known by a few that the company reached big and fell even bigger in the Dotcom Crash of the year 2000, but which growing Internet-focused company wasn’t experiencing great hardships at that time? Yet, could there be clues from those years which could be relevant today, to where the fate of MicroStrategy is heading? Let’s blow away the dust, break the crypt open and see what the passing of decades has caused to be all but forgotten.

The Data Miners

Starting out as a software company helping other companies make strategic decisions based on large amounts of accumulated data, MicroStrategy had enjoyed considerable interest and growth since it went public in 1998. CEO Michael Saylor had aimed at going public at $6 per share, had filed for $8–10 per share, sold the stock at $12 per share, only to see it rapidly continue all the way up to $46 per share. The appetite for intelligently utilizing digital data was, at this time, enormous. As an example, fast food restaurant clients could, by using MicroStrategy’s software analytics services, understand customer preferences within a geographical context; a customer in Florida was less likely to purchase a certain product than a customer in Chicago, given local circumstances. In a world where the customer is king, predicting what they actually wanted, when, and how, was profits in the making.

So with Internet usage growing exponentially in 1999, Saylor thought it was time to ramp up his vison of the digital disruption of the economy. By analyzing and processing data in real-time, MicroStrategy now wanted to deliver a service which could feed useful information, not just to large companies, but to the public. The product, an anywhere personal information network called Strategy.com, was to be offered for a small monthly fee — today a very common model for software companies — and was therefore arguably ahead of its time. Starting modestly, the service was initially to focus on sending out useful information on fickle changes in financial markets to phones, pagers and other outlets. But the goal was more far-reaching than that — when the Washington Post asked Michael Saylor for more details on his vision, he simply noted that “I believe in fate, but all things being equal, I’d rather not be standing in front of a truck when it comes down the street.” With the sprawling information network and with the help of ear-pieces, civilians would be able to receive warnings of an ongoing robbery in the street ahead of them, drivers would receive proactive, intelligent heads-ups about traffic jams before finding themselves in one, and athletes would receive real-time data on weather approaching the game field. Michael Saylor, characteristically, painted a dramatic picture:

“Take the police database in D.C. loaded into a network and then call me on the phone when there’s a robbery in my neighborhood going on right now. Don’t walk the dog, right now. There are police with sirens and shotguns running around in your neighborhood looking for three guys with knives. Right now.”

The service, in other words, would help make life both easier and safer, with the help of a never-ending tsunami of intelligently processed data. Saylor, having observed the success Amazon had built by utilizing the personalized data of customers, noted casually in an interview, “So we started to ask the question ‘How do we get embedded into everyone’s life?’”. As the theory of the new business was reaching completion, Saylor now sought a $100 million investment, about the size of the company’s annual revenues, to bring it to market.

“Proactive Intelligence”

Though a somewhat vague term, the company in other words wanted to bet on “proactive intelligence”. Adding to the examples above, Michael Saylor in another interview brought up the subject of fraud, and how an intelligent software could help mitigate it. In his example, a client is notified about the strange movement of funds from one account to another, followed by an automated text whether or not the client wants to cancel the transaction. It is not hard to see the advantages of such proactive warnings, and they are in fact implemented in multiple forms in today’s digitized economy. But in a way which would later become distinctive of Michael Saylor, he couldn’t help adding that his company was “to take everything from being unintelligent to intelligence…”, and that MicroStrategy was not an ”Internet company”, but an “intelligence company”. That also included disrupting the massive medical insurance industry with the anonymous processing of customer data. The idea that almost all data could be gathered and properly processed for all sorts of clients was a driving force in the appreciation of the value of MicroStrategy shares. Strategy.com was such a bold attempt in these early times of the internet, so all-encompassing, that it was hard to comprehend the potential ramifications stemming from a success of it. If the company could enhance data from hospitals, police stations, stock markets etc. in real-time, there seemed to be no limit to how valuable the output of the algorithms could be. Michael Saylor himself confidently stated that his system ultimately was going to “purge ignorance from the planet”.

On a question whether or not going public with his company had changed him, Michael Saylor answered:

“I think it’s made me better. It’s forced me to deal with more constituencies. It teaches you some things. Like integrity, for instance. In a public-company world, your word really means something. When you’re private you say, I’m going to do this, and if it doesn’t happen it doesn’t matter. In the public world, you say you’re going to do it, you have to do it. In the public world there’s a difference between 11:59 and 12:01, the last day of March. There’s a tangible difference. One of them is you go to jail if the thing gets signed at 12:01. One of them is the stock is up $500 million and the other one is you’ve just torched the life and livelihood of a thousand families. One minute.”

Finishing up the Washington Post interview, he predicted his company would eventually reach $10–20 billion in annual revenue. And at the time, perhaps the prediction did not sound altogether unreasonable. Saylor had after all confidently stated that “I think my software is going to become so ubiquitous, so essential, that if it stops working, there will be riots. […]. I mean that literally. I mean that people will die this year because they didn’t buy my software.” Shares continued to climb in 1999, and in the beginning of the ominous year 2000 the company had become one of the most admired in the Washington region. Shares rose ever higher, and Michael Saylor threw grand parties at his Florida mansion. A plan to build a massive 50-acre Versailles was drafted. But the celebrations and toasts to new times were not to last long.

Company Shares Implode

In March, MicroStrategy felt compelled to adapt to new accounting standards put in place a few years earlier to better reflect the reality of the operations of a growing number of software companies in the nation. In practice, this meant that MicroStrategy had overstated its revenues two years in a row, and what was priorly booked as profitable years now turned deeply red. The original 1999 annual profit of $12.6 million was now restated as a loss of as much as $40 million. In a market sensitive to even small misses on investor expectations, the company shares crashed about 62% in a day, reducing Michael Saylor’s net worth by multiple billions of dollars — one of the largest daily personal losses in the world to that date. PricewaterhouseCoopers, the company’s auditors, had put a stamp of approval on past reporting, so the change did not exactly stem from a complete failure in that regard.

What had happened with the revenue discrepancy was extremely ironic; a late-night business deal had been struck with the large technology company NCR Corp on September 30th, 1999, but as no flow of goods or money occurred that day, NCR booked it in the fourth quarter of the year, while MicroStrategy booked it in the third quarter. In other words, Michael Saylor had found himself in exactly the situation he so much dreaded during the interviews with the Washington Post earlier in the summer. Had he not booked the revenues stemming from the business deal in the third quarter, the company shares would likely have crashed and severely complicated the funding of the company’s ongoing Strategy.com transformation. Instead, Saylor and the other higher-ups in the company saw shares increase 72% in value since that fateful meeting, paving the way for large sales of their personal holdings for a total of $82 million during the period. That was more than four times the value of previous insider sales since going public.

Not only was the revenue booked wrongly, but the deal also included the promise by MicroStrategy to purchase a business unit and some software from NCR, thus netting the total effect of the deal on revenues. “Revenue washing” is a well-established way to artificially inflate booked revenues while not being properly reflected in actual business activity. So, three problems were now glaringly obvious to investors who had just lost a lot of money: revenues had likely been booked in the wrong quarter, the $27.5 million NCR deal involved a tit-for-tat purchase of about $25 million, and the MicroStrategy executives and board members had sold shares that they likely knew were severely overvalued, to the open market.

While the details of the NCR deal came to light, a later deal with Primark Corp. to distribute financial information to investors, also attracted the eyes of market analysts. Quite incredibly, Michael Saylor seems to have found himself in the situation yet again, where a business deal was signed and booked in the fourth quarter of 1999, while it was actually carried out and paid for in the first quarter the year after. Investors, oblivious at the time to any wrongdoings in the two separate business deals, had bid up shares above $300 before all the accounting issues came to light. All this seems to have become too much for the SEC, which promptly launched an investigation into the company. It eventually compelled MicroStrategy to admit to booking revenues wrong over the last three years rather than the last two. At this time, shares were down more than 80% since their all-time high. Michael Saylor’s company stake had dropped in value, from $13.6 billion to $1.7 billion.

The Strategy.com investment never materialized as the company failed to get approval for new share issuance and sales before the value of the shares cratered in March 2000. A plan to raise up to $2 billion, then the largest stock offering in software industry history, came to nothing. Michael Saylor’s vision of a large proactive intelligence network was put on ice, and the company returned to its tried ways of conventional data mining. The abrupt fall was distinct enough to prompt James Cramer, columnist for TheStreet.com, to state that “This one popped the bubble. MicroStrategy forever changed the Internet mania.”

The rise and fall of MicroStrategy would, except for the whispers in obscure investor circles, eventually be followed by a long silence. But the years passed, and Bitcoin finally entered the world and caused an ever-larger stir around the globe. Saylor initially discarded the phenomenon, writing that “#Bitcoin days are numbered. It seems like just a matter of time before it suffers the same fate as online gambling.” But as the network grew, and after various decadent money printing schemes had been put in motion by governments in 2020, something seems to have changed within Michael Saylor. A growing opportunity now lay before him and his company, perhaps larger than all his prior visions put together, as a new untrodden path opened under the gaze of an orange sun.

MicroStrategy entered its Bitcoin Exploration phase simply as an enterprise analytics software and services company with a checkered past and with fading growth. There is nothing wrong with that — the company made small profits on the capital it applied to the purpose. Few assumed much future growth in revenues, and valued the company shares accordingly. Total revenues for the second quarter of 2020 were reported as $110.6 million, a 6.1% decrease from the year before. In that same report (10-Q, 2020–06–30), however, the word “Bitcoin” appeared for the first time. What followed was the company with its investors, under the surprised gaze of its peers, boldly moving away from competing with IBM, Microsoft, Oracle, and Salesforce, to standing alone at the door to the growing Bitcoin sector. The report, after announcing the buyback of $250M worth of shares through a modified Dutch Auction, added that:

MicroStrategy will seek to invest up to another $250 million over the next 12 months in one or more alternative investments or assets, which may include stocks, bonds, commodities such as gold, digital assets such as bitcoin, or other asset types. (10-Q, 2020–06–30, Exhibit 99.1.)

In August 2020, an 8-K document (8-K, 2020–08–11) was filed at the SEC, announcing the purchase of 21,454 Bitcoin at an aggregate purchase price of $250.0 million. The risk factors section of the previously published quarterly report was amended, and Saylor noted in the document that:

“Bitcoin is digital gold — harder, stronger, faster, and smarter than any money that has preceded it. We expect its value to accrete with advances in technology, expanding adoption, and the network effect that has fueled the rise of so many category killers in the modern era.” (8-K, 2020–08–11, Exhibit 99.1.)

The conventional Treasury Reserve Policy of the company was updated with a Bitcoin-focus in September the same year, with a new 8-K filing. And after the Q2 report had mentioned the word “Bitcoin” once, the Q3 report mentioned it 154 times. The air in the company was now thick with change.

Steering the Helm

During the third quarter of 2020, MicroStrategy ended up owning about 38,250 Bitcoin, purchased for $425 million ($11,111 per Bitcoin). This from a considerable portion of the company cash position. By September 30, 2020, MicroStrategy had cash and cash equivalents and short-term investments of $52.7 million, compared to $565.6 million by the end of 2019. On the 4th of December 2020, MicroStrategy bought 2,574 more Bitcoin (8-K, 2020–12–04). For the annual report of that year, the shift in strategy is again palpable, and the mention of raising capital for the purpose of buying Bitcoin through debt or share issuance could be spotted for the first time:

MicroStrategy® pursues two corporate strategies in the operation of its business. One strategy is to grow our enterprise analytics software business and the other strategy is to acquire and hold bitcoin. […]. [A]nd we may from time to time, subject to market conditions, issue debt or equity securities in capital raising transactions with the objective of using the proceeds to purchase bitcoin. (10-K, for the fiscal year ended December 31, 2020, p.5.)

Approximately 70,469 Bitcoin were purchased in total in the year 2020, indicating many were purchased at the very end of the year. All Bitcoin now had an average purchase price of approximately $15,964 per coin. The later batches of purchases were made with an issuance of $650 million principal amount of 0.75% convertible senior notes due 2025. The issuance was announced in December 2020, and had a conversion price of about $397.99 ($39.799 for the post-split shares of August 2024) and thus MicroStrategy went from purchasing the new volatile asset with surplus cash, to purchasing it with convertible debt. One of the first things incredulous onlookers reacted to was the low interest rate for the bonds — something which we will return to later.

Officially Adopting a New Strategy

In early 2021, MicroStrategy, already operating under its amended Treasury Reserve Policy, officially adopted a Bitcoin Acquisition Strategy, further strengthening that focus. Within weeks, a new convertible bond issue was announced (8-K, 2021–02–16), this time of up to $1,050 million of 0% convertible senior notes due 2027. Though larger than the first issue, its zero coupon meant the lender’s full focus was on the equity component of the convertible bond. The focus of the borrower was, as we know, to purchase more Bitcoin with the proceeds. Conversion price of the bonds was priced at about $1,432, meaning about $143 in 2024 post-split shares. After the purchase of more Bitcoin, the number of Bitcoin per share climbed above 0.001. For the first time, investors in the company had to contemplate the nuances of MicroStrategy having issued multiple types of convertible bonds, as the conversion into shares of one issue could affect the parameters allowing conversion for other issues. Some confusion arose out of this, which we will speak more of later.

The Third Issue — Regular Bonds

In June 2021, a third bond issue was announced, this time of $500 million worth of 6.125% senior secured notes due 2028. This being a conventional straight bond, it can be observed how the market viewed the risk of MicroStrategy’s Bitcoin Acquisition Strategy, through the coupon payments. Herein lies the first clue in how to view the low coupon payments of the first two issues. Were the earlier bonds really as cheap as they seemed at a first glance? It was a relevant question that investors could now ponder. At the time of this third bond issue MicroStrategy owned 92,079 Bitcoin, and now more could be acquired.

A Long Period of Accumulation & The Fourth Issue

As of January 31, 2022, MicroStrategy held approximately 125,051 Bitcoin (8-K, 2022–02–01) which were acquired at an average purchase price of about $30,200 per coin. On the 29th of March 2022, a fourth debt issue was announced, this time with Silvergate Bank, of $205 million secured by Bitcoin held in MicroStrategy’s collateral account. The loan had a floating rate equal to the SOFR 30 Day Average plus 3.70%, with a floor of 3.75%. The collateral was set at double the loaned amount, $410 million. Saylor concluded that “the SEN Leverage loan gives us an opportunity to further our position as the leading public company investor in bitcoin.” The Silvergate loan was paid back in March 2023 at a discount (8-K, 2023–03–24), due to the interest rate climbing up towards 8%. The payment could be made by the company issuing new MicroStrategy shares, though not yet at a premium to net assets. This meant that three bond issues, of which two were convertible, were still outstanding.

In the 2022 annual report the company’s Bitcoin Acquisition Strategy had clearly overtaken any focus on the software business, as seen in the number of mentions of “Bitcoin”, and in the stated order of company objectives. As of February 15, 2023, MicroStrategy held approximately 132,500 Bitcoin with an average purchase price of approximately $30,137 per Bitcoin. Further purchases that year were funded mainly by the issuance and sale of new shares (8-K, 2023–06–28). As MicroStrategy at the time traded near its net asset valuation, meaning its cash and Bitcoin holdings, the share issuance and purchases were not much affecting the company capital structure. Not until the end of 2023 did the Bitcoin price recover enough to surpass MicroStrategy‘s cost basis. At that time, the company held 189,150 Bitcoin, with an average purchase price of $31,168 per coin.

The NAV Premium Increases

Starting in 2024, the market valuation of MicroStrategy in proportion to its Bitcoin holdings quickly increased to about two. This meant that the implied valuation of a Bitcoin held by the company was double that of a Bitcoin trading at exchanges. The software business, now a very small part of the company’s dealings, had become more or less irrelevant and could share no consideration in the total valuation. Investors were bidding on shares because of the Bitcoin exposure, and nothing else. Before the approval of the Bitcoin ETF in January 2024, a popular narrative circulated around the assumption that the premium earlier had manifested itself due to MicroStrategy offering the only possible exposure to Bitcoin for various institutional investors. MicroStrategy mentioned this dynamic in its annual report for 2023:

On January 10, 2024, the SEC approved the listing and trading of spot bitcoin ETPs, the shares of which can be sold in public offerings and are traded on U.S. national securities exchanges. The approved ETPs commenced trading directly to the public on January 11, 2024, with a trading volume of $4.6 billion on the first trading day. On January 11, 2024, and in the subsequent days following the SEC’s approval of the listing and trading of spot bitcoin ETPs, the trading price of our shares of class A common stock declined significantly relative to the value of our bitcoin. To the extent investors view our class A common stock as providing exposure to bitcoin, it is possible that the value of our class A common stock may also have included a premium over the value of our bitcoin due to the prior scarcity of traditional investment vehicles providing investment exposure to bitcoin, and that the value declined due to investors now having a greater range of options to gain exposure to bitcoin and investors choosing to gain such exposure through ETPs rather than our class A common stock. (10-K, for the fiscal year ended December 31, 2023, pp. 24–25.)

As the premium to the company’s net asset value quickly recovered and continued to increase in the following months, despite the approval, some went in search of other explanations or narratives. The quickly increasing share price mostly dissuaded such considerations, however, and optimism reigned supreme.

More Bond Issues and the Bitcoin Development Company

While some mulled over the rising premium to net asset value, the company issued more convertible debt for the first time in almost three years (8-K, 2024–03–11). $800 million worth of unsecured convertible senior notes due 2030 with a 0.625% interest rate meant more Bitcoin could be accumulated with the proceeds. Here, for the first time in a long time, could MicroStrategy make use of the premium to its net asset value. A few days later, another issue was made of $600 million worth of unsecured convertible senior notes due 2031 with a 0.875% interest rate (8-K, 2024–03–19). As of February 14, 2024, the company held about 190,000 Bitcoin, with a purchase price of $31,224 per coin.

MicroStrategy had now officially morphed into the “world’s first Bitcoin development company”, according to its annual report for 2023 (10-K, 2023, p.7). What, exactly, this entailed is hard to determine, but a qualified guess is an internal focus was shifting towards building blockchain analytics tools, first layer Bitcoin clients, Lightning Network clients, and so on. Any Bitcoin software useful to the entity running it, could fetch a continuous yield as real as the yield from Microsoft software.

As of April 26, MicroStrategy had accumulated 214,400 Bitcoin, meaning the milestone of owning more than 1% of all supply had finally been achieved. The coins were acquired for approximately $35,180 per coin. Total revenues, per the Q1 report (8-K, 2024–04–29), was $115.2 million, down 5% year-over-year, further emphasizing the fading relevance of the non-Bitcoin parts of the company.

In June, a fifth convertible bond issue was conducted (8-K, 2024–06–17). The bonds were $800 million worth of unsecured convertible senior notes due 2032 with a 2.25% interest rate. Almost simultaneously, the company’s first convertible bond issue with a principal of $650M and a conversion price below the current share price, was prematurely redeemed by converting it all into equity (8-K, 2024–06–13). Capital structure decisions taken three and a half years ago now made themselves known. Though more Bitcoin were purchased with the proceeds from the fifth convertible bond issue, the Bitcoin per share ratio seems to have increased only marginally at this time.

Stock Split & Small Capital Structure Changes

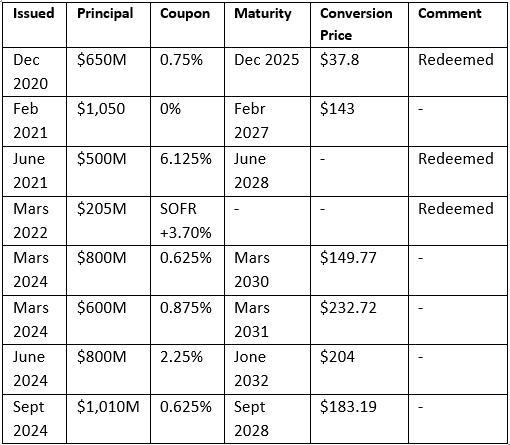

In July, MicroStrategy announced a 10-for-1 split (8-K, 2024–07–11). All debt contracts automatically changed in proportion, and the report has previously dealt with post-split conversion prices for the convenience of the reader. In September, the company announced Bitcoin purchases for over $1 billion, conducted with proceeds from share issuance (8-K, 2024–09–13). This meant it continued to take advantage of the premium to net asset value, and its accelerating accumulation now reached 244,800 Bitcoin. Also in September, a sixth convertible bond issue was planned, to raise enough funds to redeem the 6.125% 2028 Senior Secured Notes issued in June 2021 (8-K, 2024–09–16). The move is in line with a capital structure optimization strategy, as the new convertible bond issue would be done with shares at a premium. The issue was $1.01 billion aggregate principal amount of 0.625% convertible senior notes due 2028 with a $183.19 conversion price, and all the secured bonds of 6.125% were consequently redeemed — a good move by the MicroStrategy team. The company’s bond schedule now looked something like the following:

The exploration phase was concluded; the company had now found its orange path to success, and it lay not in Bitcoin- or non-Bitcoin software development, but in pursuing accretive treasury operations.

The “21/21 Plan” of the Bitcoin Treasury Company

In a historical announcement in connection with the 2024 Q3 earnings report (10-K, 2024–10–31), the company, in a hat-tip to Satoshi, announced the goal of a $21 billion at-the-market (ATM) equity offering — meaning share issuance — as well as a target of raising $21 billion using fixed-income securities. The plan was to conclude over the course of the next three years. At the time of the launch of the plan the debt approximately amounted to a $4.26 billion principal.

The rapid shift from being a Bitcoin Development Company to a Bitcoin Treasury Company is clearly seen in the change of the Business Overview section of the Q2 report and the Q3 report. The latter, having pushed all software development, on Bitcoin or otherwise, to the background, now stated:

MicroStrategy® is the world’s first and largest Bitcoin Treasury Company. We are a publicly traded company that has adopted Bitcoin as our primary treasury reserve asset. By using proceeds from equity and debt financings, as well as cash flows from our operations, we strategically accumulate Bitcoin and advocate for its role as digital capital. Our treasury strategy is designed to provide investors varying degrees of economic exposure to Bitcoin by offering a range of securities, including equity and fixed income instruments. In addition, we provide industry-leading AI-powered enterprise analytics software, advancing our vision of Intelligence Everywhere. We leverage our development capabilities to explore innovation in Bitcoin applications, integrating analytics expertise with our commitment to digital asset growth. We believe our combination of operational excellence, strategic Bitcoin reserve, and focus on technological innovation positions us as a leader in both the digital asset and enterprise analytics sectors, offering a unique opportunity for long-term value creation. (10-K, 2024–10–31, p.26.)

What a Bitcoin Treasury Company meant in practice was simultaneously explained by the new MicroStrategy CEO Phong Le, in an 8K-filing:

“As a Bitcoin Treasury Company, we plan to use the additional capital to buy more bitcoin as a treasury reserve asset in a manner that will allow us to achieve higher BTC Yield.” (8-K, 2024–10–30, Exhibit 99.1.)

So with yet another rebranding of the business to a Bitcoin Treasury company, with a stated goal to create Bitcoin yield — a metric first spotted in September (8-K, 2024–09–16) — MicroStrategy entered The Golden Age in its pursuit of a place in the history books. Now fully focused on extracting Bitcoin yield to the fullest extent, the company defined the yield as,

BTC Yield is a key performance indicator (“KPI”) that represents the % change period-to-period of the ratio between the Company’s bitcoin holdings and its Assumed Diluted Shares Outstanding. Assumed Diluted Shares Outstanding refers to the aggregate of the Company’s actual shares of common stock outstanding as of the end of each period plus all additional shares that would result from the assumed conversion of all outstanding convertible notes, exercise of all outstanding stock option awards, and settlement of all outstanding restricted stock units and performance stock units. (8-K, 2024–10–30, Exhibit 99.1.)

The Bitcoin yield could come from multiple sources, and MicroStrategy has to this date utilized some of them more than others. By selling shares through ATM offerings at a premium to net asset value, the Bitcoin yield could come out of the proceeds from buyers of the newly issued shares. The total Bitcoin yield is in that situation precisely equal to the total premium paid by these marginal buyers. In other words, it is not inherent to the ATM offering itself, but is provided from outside the corporate structure.

By raising funds through convertible bond issues, a positive Bitcoin yield could similarly come from Bitcoin purchases made with the proceeds from buyers of the bonds, while a negative yield could later materialize should the convertible bonds not convert in the future. By issuing straight bonds, a positive Bitcoin yield could also come from the immediate proceeds, but would very likely turn negative in the future when the debt had to be repaid. This last method has been employed only once by the company (twice if counting the short-lived Silvergate Bank issue). The first two methods are much more lucrative with shares trading at a premium to company net assets.

If shares are at a premium, this constitutes an arbitrage opportunity for MicroStrategy when utilizing the ATM offerings. Though not strictly an arbitrage, convertible bonds issued while the company trades at a premium create opportunities as well. If the bond holders in the future convert the bonds at inflated conversion prices, they receive newly issued shares at a price often above the company’s net asset value, and the generated Bitcoin yield would then stand in proportion to this premium. All this considered, the company’s 21/21 Plan logically focused on the first two types of treasury operations; more shares and more convertible bonds were to be issued.

The Plan Proceeds

Within two weeks of the bold 21/21 Plan MicroStrategy had bought approximately 27,200 Bitcoin for $2.03 billion, at an average price of approximately $74,463 per coin (8-K, 2024–11–12, Item 8.01). The purchase seems however to have been made by depleting the previously undertaken ATM offerings, and any new purchase was now to be made through the new plan.

On the 18th of November, we could first see such a filing (8-K, 2024–11–18). The company had bought 51,780 new Bitcoin for $4.6 billion in cash, at an average price of about $88,627 per coin. This catapulted the company’s Bitcoin holdings to over 300,000 for the first time, marking yet another milestone. Over 13 million new shares were issued to fund this. Two days later, on the 20th of November, the company’s largest convertible bond issue to date was announced (8-K, 2024–11–20). $3 billion was raised at 0%, with a conversion price of $672.40 at 55% premium, and with maturity in 2029. This meant that both the ATM offering arm and the convertible debt arm of the 21/21 Plan were being utilized. Issuance now occurred at a pace hard to keep up with, as the MicroStrategy team wanted to take advantage of the company’s shares trading at a premium to net assets. On the 2nd of December the company’s Bitcoin holdings reached above 400,000 for the first time as more shares had been issued and sold (8-K, 2024–12–02). Bitcoin yield for 2024 was now enormous, and about half of the ATM offering arm of the 21/21 Plan had been exhausted.

Rationalizing the Premium

With Bitcoin yield surpassing even the highest company estimates of the Q3-report, everything was going better than planned. The new shares hitting the bid on enthusiastic buyers in record numbers did nothing to dent the premium to net assets — in fact, November saw net asset multiples at the highest levels in years. With shares trading at 200% above net asset value, this meant the MicroStrategy treasury team could issue and sell shares representing ownership of 1 Bitcoin, to fund the purchase of 3 new Bitcoin. Net proceeds, 2 Bitcoin, would then be the Bitcoin yield, divided and given to all shareholders in proportion to ownership of the company. The 2 Bitcoin would be the Bitcoin per share increase in aggregate.

There are a number of reasons the company could extract Bitcoin yield at the pace it now was doing. Investors argued that MicroStrategy’s debt was cheap. And indeed, it borrowed billions of dollars and paid often less than 1% in annual coupons — far below official inflation numbers. In a world swimming in surplus cash, it seemed lenders were willing to part with capital at record low interest rates. While this debt mostly came in the form of convertible bonds, it was argued that the company would not suffer dilution, because the debt was accretive with shares trading at a premium to net asset value. In fact, investors clamored for this type of dilution, seeing as the Bitcoin per share metric could continuously increase.

The premium to net assets, it was also argued, came from the fact that MicroStrategy was a “levered play” on Bitcoin. With ETFs, investors either had to suffer the dull movements of an asset without leverage, or face the large risks and volatility decay of levered ETFs. With MicroStrategy, you could get a levered upside, but withstand being wiped out in prolonged downturns, as proven in 2022 and 2023. Because of the company’s flexibility to use “intelligent leverage”, the premium seemed reasonable to any thrill-seeking bitcoiner.

It was argued that the premium also originated from “regulatory arbitrage”. With this, investors pointed to the fact that the company helped facilitate exposure to Bitcoin for institutional portfolios not allowed to own Bitcoin, or even an ETF, outright. The bond market, very large but also very restricted, had with MicroStrategy’s innovative convertible bonds finally a way to get exposure to Bitcoin on the upside, while being protected to the downside through the bond “floor” — the principal amount. It did not seem unreasonable to assume that if MicroStrategy now was the main actor providing such financial products, it of course should reap profits from the operations, manifesting itself in the share premium.

At this time, the popular narrative of an “infinite money glitch” was used to rationalize a premium as well. And on the face of it, it seemed reasonable. MicroStrategy could issue convertible bonds with conversion price at a premium and buy Bitcoin with the proceeds. As the price of Bitcoin increased, the company’s fundamental value increased, meaning shares increased in value as well. With the higher valued shares, the company could now issue even more bonds, in a seemingly circular flywheel dynamic. Another version of this narrative is the notion that MicroStrategy conducts a “speculative attack” on the fiat currencies.

So when the 21/21 Plan was initiated, and with the above considerations in mind, investors could foresee large Bitcoin yield payments to the shareholder owned company coffers. The shares increased in price accordingly. Within less than a month, Saylor could announce that the company had achieved a Bitcoin yield surpassing 40% year-to-date — an enormous number compared to the yield of traditional finance. Within five weeks since launch, the year-to-date Bitcoin yield had surpassed 60%. Everything crushed expectations, and it appeared to many as if the Bitcoin yield could soon be extracted in a near unlimited supply as a stagnant fiat economy realigned its rusting axis with a new, pristine Bitcoin foundation.

While the ATM offering activities were absorbed by the market happily enough, the demand for the company’s convertible bond issues seemed near bottomless as well as they grew ever larger in size. Michael Saylor had become the uncontested hero of many bitcoiners. Having accumulated the single largest Bitcoin hoard the world had ever seen, nothing could stop the company’s ascendancy. Or could it?

While foreshadowing clearly can be read between the lines of the earlier rationalizations of MicroStrategy’s valuation, it should be remembered that all this mainly took place in a market where equities reached all time highs, gold reached all time highs, and finally, Bitcoin and MicroStrategy reached all time highs. Whatever unstructured thoughts investors had in their heads all seemed vindicated by the reality of riches quickly made. No one had much appetite to consider what was happening through a lens of first principles, where complex financial dynamics are broken down in smaller and smaller parts that you know to be true. As the premium on MicroStrategy shares to net assets increased and not decreased with the accelerating ATM offerings, it was simply accepted by some as a truth within the asset, rather than as a contradiction in need of logical inquiry through laws of finance. Let us now go through many of the popular narratives and see what substance they all really hold.

“Don’t forget the dirt cheap loan (.063%) he secured for 6 or 700M.” — Reddit user #1.

“Imagine loaning someone 700M and 0% interest instead of buying btc.” — Reddit user #2.

It is an easy mistake to make, in assuming that a low interest rate on a debt instrument means it is cheap. But because MicroStrategy’s many bond issues for the purpose of buying Bitcoin are convertible to equity at a predefined conversion price, a low interest rate on the bonds can’t be compared with interest rates on normal loans. It should go without saying that if lenders demand more than 4% from the US Government, they will not simultaneously demand less than 1% from MicroStrategy — a company with decreasing revenues and where the main business now consists of buying and holding Bitcoin.

Convertible bonds are hybrid securities with debt-like and equity-like features. They are in practice regular bonds with free embedded call options, meaning the price (also known as the premium) of the call options makes up for the lender’s loss of a high yield, or coupons. Here is a simplified illustration of a convertible bond’s value at maturity:

In other words, with the convertible bond issues, MicroStrategy had not found a philosopher’s stone, but could bypass a high interest rate on its debt only by giving away upside as the bonds convert into equity at conversion price. Just because investors wish the company could borrow cheaply, does not make it so. The company’s straight bond issue in June 2021 was priced at 6.125% coupon payments, giving a truer indication of the company’s cost of capital.

To further emphasize the point, consider for a second what could happen if MicroStrategy were to move the maturity date further away, or lower the conversion price of the convertible bond issue, meaning the strike price of the embedded call option. A situation could then arise where a lender pays MicroStrategy for the privilege of lending to the risky company! The yield on the bonds turns negative. While seemingly unreasonable at first glance, it is simply a result of a large prepayment by MicroStrategy in the form of the free call options, for the privilege of “borrowing cheaply”. We can conclude that the narrative breaks down, yet it is repeated regularly by many MicroStrategy investors every time another convertible bond issue is undertaken.

Some investors seem to have misunderstood another aspect of the company’s convertible bonds. It concerns the notion that the company is protected from dilution due to how the convertible bond issues are structured. And it is not a surprise that many are confused. Consider for example the wording from the very first company announcement of a new issue: “Subject to certain conditions, on or after December 20, 2023, MicroStrategy may redeem for cash all or a portion of the notes at a redemption price equal to 100% of the principal amount of the notes to be redeemed, plus accrued and unpaid interest, if any […].” This sounds like a great deal to MicroStrategy — not so much for the lender. But this is common wording for convertible bonds. It does not mean that if the share price surpasses the higher conversion price stipulated for the convertible bond, MicroStrategy can somehow redeem the bonds just before they were to convert into equity (and as a consequence stop the dilution of existing shareholders). The wording is to force the bond holder to convert to equity, should that not happen for some reason. Certain bond investors may for example be market neutral hedge funds that short sell the shares while buying the convertible bonds. Many of them would rather the bonds not quickly convert — they seek volatility to profit from gamma trading.

In practice, non-conversion is a situation which should never occur if conversion conditions have been fulfilled. Given a choice, bond holders of course want the higher valued shares at conversion price, rather than the initial principal amount plus a bit of interest. Looking at an SEC filing from MicroStrategy three and a half years after the first convertible bonds were issued, when early conversion of these notes to new shares actually took place, further strengthens this understanding:

On June 13, 2024, the Company announced that it delivered a notice of full redemption (the “Notice”) to the trustee of the Company’s outstanding 0.750% Convertible Senior Notes due 2025 (the “2025 Notes”). The aggregate principal amount of the 2025 Notes being redeemed is $650.0 million, which is equal to the current aggregate principal amount of 2025 Notes outstanding and held by investors. The Notice calls for the redemption of all of the outstanding 2025 Notes (the “Redemption”) on July 15, 2024 (the “Redemption Date”), at a redemption price equal to 100% of the principal amount of the 2025 Notes to be redeemed, plus accrued and unpaid interest, if any, to but excluding the Redemption Date, unless earlier converted.

As a result of the delivery of the Notice, at any time prior to 5:00 p.m., New York City time, on July 11, 2024, the 2025 Notes are convertible, at the option of the holders of the 2025 Notes, at the applicable conversion rate of 2.5126 shares of the Company’s class A common stock per $1,000 principal amount (reflecting a conversion price of $397.99 per share). (8-K, 2024–06–13)

In summary, if the share price increases, there will be conversion of these debt instruments into equity, meaning new shares. BitMEX research understood this to be the case as well while recently investigating the company’s capital structure. MicroStrategy is not protected from dilution — if it were, the lenders in the first convertible bond issue would not agree to a 0.75% coupon, but would likely demand something closer to a 6–10% coupon.

As MicroStrategy issued more convertible debt, a question arose as to whether the potential dilution of equity by some convertible bonds affects the other convertible bonds or not. The answer lies in anti-dilutionary clauses. Consider that for convertible bonds the conversion ratio = principal amount/conversion price. Anti-dilutionary clauses means that the conversion ratio increases in proportion to dilution, meaning the conversion price decreases in proportion (as principal amount stays the same). A 5% dilution from one bond converting into equity, in other words, lowers the conversion price of the other bonds accordingly. Another way to view it is that the “strike prices” of all other issued call options, as baked into the convertible bonds, decrease in proportion to dilution. If there were no anti-dilutionary clauses, the company could simply issue shares and sell them to keep the share price from ever reaching the conversion price stipulated for the various issues. Lenders would for obvious reasons not accept such a convertible bond at low yield, because the free call option would be engineered to expire worthless. Again, they would demand perhaps a 6–10% coupon, not less than 1%, which has been the case for MicroStrategy.

“Buy Bitcoin, Bitcoin goes up, Stock is tied to Bitcoin, Stock goes up, Sell stock, use cash to buy more Bitcoin, repeat. Infinite money glitch.” — Reddit user

Somewhat related to the narrative of “cheap debt”, is the popular claim that MicroStrategy has found an “infinite money glitch”. An investor may for example argue that MicroStrategy can issue shares or convertible debt, sell it, purchase Bitcoin with the proceeds, the price of Bitcoin increases, the MicroStrategy share price increases as a function of the underlying Bitcoin holdings, and the company issues and sells even more convertible debt. And round it goes. But MicroStrategy does not have control over the Bitcoin price; the size of the issues is dwarfed by Bitcoin’s total market capitalization. Whatever buy pressure the company can apply on the Bitcoin price through these treasury operations, is multiple times offset by the sell pressure applied by the new issuance on the MicroStrategy share price. Note that the sell pressure is immediate if from share issuance or from convertible bond issues bought by market neutral hedge funds. The sell pressure is latent and may occur in the future if from convertible bond issues bought by regulatory restricted investors seeking Bitcoin exposure in roundabout ways. But there is ultimately no way around it all, unless the company were to pursue regular bond issuance, meaning the total risk undertaken by the company increases in proportion to the leverage.

So any “infinite money glitch”, could just as well transform into permanent monetary losses should the company have to liquidate parts of its Bitcoin holdings or raise funds in a depressed market environment as the convertible bonds finally mature below conversion price. In other words, there is no glitch, but mainly debt-fueled risk taking which may give a certain boost to the upside, or a fatal blow to the downside. It remains to be seen how current treasury operations will affect the company when times are bad. The potential for creating shareholder value through capital structure shenanigans must obviously be discounted by the very real risk of future fire sales. “It is going up forever Laura”, though a catchy meme, is not economic reality.

With the continued issuance of shares through ATM offerings to purchase more Bitcoin, onlookers thought that Saylor conducted some sort of magic trick, where he with no additional risk could increase the company’s Bitcoin per share ratio. It needs to be stressed that the issuance in 2023 and early 2024 was conducted with little to no premium to net asset value. In practice, this meant that any Bitcoin purchase through such a measure is fully offset by the dilution of the shares. The company may own 10% more Bitcoin after everything has been concluded, but any old shareholder has been diluted by about 10% as well. The Bitcoin per share ratio can’t increase this way — it is only possible with instruments such as regular bonds (meaning higher risk), convertible bonds (meaning higher risk), or with the issuance of new shares if the premium to net asset value is above one.

Being generous to the prominent bitcoiners discussing the dynamics in the referenced video, they do in fact mention issuance during high price to earnings (P/E) ratios. The P/E ratio for MicroStrategy is currently irrelevant, however, and what they need to look at is, as has been pointed out, the premium to net asset value. MicroStrategy has no earnings to speak of, in relation to its high market valuation. Its P/E can in the future increase or decrease while booking unrealized gains or losses on the Bitcoin it owns, but that does not mean it is time to issue shares and buy more Bitcoin (or sell Bitcoin to buy back shares). The company should only consider such issuance if the premium has climbed some way above one. And such a scenario, in fact, happened a few months after the above discussion.

It can be added here that the same dynamic holds true for convertible bond issuance. MicroStrategy can, if shares trade at a premium to net asset value, issue and sell the convertible bonds with a high conversion price, to the detriment of potential buyers of the bonds. As the shares trade at a premium, it is evident that the bond conversion price must be at an even higher premium, causing conversion conditions to be unusually hard to meet. As with the ATM offerings, MicroStrategy is better off issuing convertible debt when shares are at a premium. This share premium should not be assumed, however, but that will be discussed later in the report.

More P/E-related confusion came years later, as MicroStrategy’s treasury operations brought heaps of Bitcoin yield to excited investors. In a clever twist of definitions, Saylor took this yield to be equivalent to earnings, and from there implied an extremely high fundamental value of the company based on a “P/E ratio” as well as “earnings growth” snapshot. There were multiple things wrong with this narrative. For P/E to be relevant in company valuation, the denominator must be somewhat consistent over time. A high one-off earnings number can make any company look undervalued versus peers, but it is all an illusion should that high earning not be followed by similar numbers. MicroStrategy’s Bitcoin yield is provided mostly by retail investors buying company shares at a premium, and there is a finite supply of those. It is not honest to extrapolate temporarily high Bitcoin yield and imply the company should be valued much higher — that’s not how it works. Capturing the premium in ATM offerings is an activity with a finite lifespan, given the nature of the operation. Furthermore, part of the Bitcoin yield also stems from the convertible bond issues, and they come with a risk; the bonds may not always convert, meaning the principal amount would need to be paid back. Having then already categorized the Bitcoin yield stemming from such proceeds as earnings, is an Enron-like categorization error. The outstanding bonds in question must mature or redeem before booking the Bitcoin yield as earnings. Mark Meldrum pointed out exactly this.

“#Bitcoin is a swarm of cyber hornets serving the goddess of wisdom, feeding on the fire of truth, exponentially growing ever smarter, faster, and stronger behind a wall of encrypted energy.” — Michael Saylor

Asset Decay

While MicroStrategy’s Bitcoin accumulation strategy kicked into high gear in 2024, it was argued that Bitcoin was the best reserve asset to hold there is for a company, because it has no drag, or no decay. The asset’s low maintenance costs were compared to those of the heavy machinery of Bristol-Myers Squibb, technical monstrosities that for obvious reasons are in need of constant service and care. The comparison fails because the machinery has an inherent yield — it produces more than what it consumes, or it would not have been painstakingly constructed — whereas the Bitcoin of MicroStrategy so far is a “dead asset”, sound asleep at the custodians without any conventional yield.

While the comparison to physical capital is halting, it should be realized that even if one were to view them that way, MicroStrategy’s Bitcoin holdings still impose costs. Someone, somewhere, is paying the Bitcoin miners, or the network has no hashrate and subsequently is susceptible to DoS attacks. Assuming that it is others, and not MicroStrategy, that will bear the brunt of this cost is probably a mistake. It should also be added that MicroStrategy makes use of US custodians — the decay being the annual costs and risk of theft and confiscation there. Bitcoin is not a completely cost-less asset to own, and should not be characterized that way.

Cyber Manhattan

A master wordsmith of analogies, Michael Saylor has provided his share of comparisons as well. One of the more famous ones is that Bitcoin is a “Cyber Manhattan”, digital real estate which people should want to buy and own for a hundred years. Having accumulated a considerable portion of this digital real estate within a company framework, investors were soon to realize the true value of MicroStrategy. This comparison halts on many accounts. While painting real estate in Cyber Manhattan as immortal, as not subject to a fickle or corrupt mayor, to physical decay, to taxes, to regulations, to break-ins etc., this is first of all forgetting that all such factors can change. Many nations are already considering taxes on unrealized gains, and to prop up their own failing currencies and bonds, such assets may obviously be excluded from the tax schemes. But the most obvious difference between Bitcoin and real estate is the yield received from rental properties. This is a sector which will never go away, because investors always seek yield. Even in a hypothetical hyperbitcoinized world, investors can invest in the real estate market and earn Bitcoin yield forever. Again, Bitcoin is mostly a dead asset, as is a gold coin, or a seashell. It does not yield in itself (and shouldn’t). For yield it must first be traded for a capital good, such as ownership in factories, skyscrapers, service firms etc.

Digital Capital

Another popular but vague Saylor analogy is that the company’s Bitcoin are digital capital, and that this is something novel and exclusive in the economy. Capital are production goods — goods of higher order. They are goods that are aquired for the purpose of producing consumption goods. Any software used by companies around the globe is digital capital. Any currencies used by banks to create financial products or services are digital capital. The term is not at all exclusive to Bitcoin, and ironically, most of the time when Bitcoin owners think they hold “digital capital”, they hold the coins in cold storage, just as a gold owner may keep gold coins in a vault. If the good is not used for producing another good, then it is simply not capital. There is nothing wrong with that — not everything you own must be geared towards production.

“Don’t try to put some premium trading bullshit. Don’t try to make something up from thin air. Because all your models are fucking broken.” — MicroStrategy thought leader.

Notwithstanding the fact that the belief in a persisting premium to net asset value, or NAV, is itself a model, we are now approaching the most critical takeaways of the report. As 2024 proceeded with MicroStrategy shares exploding upward, and as the premium to the company’s net assets persisted in spite of the go-ahead of new Bitcoin instruments, some onlookers voiced their confusion about all this. Simultaneously, the popular Quant Bros duo released their first video on pre-split MicroStrategy, titled “Can MicroStrategy (MSTR) hit $10,000?”, outlining something which “the Ben Graham philosophy would just never understand”. The high valuation forecasting was based on the assumption that shares could uphold the premium. Together with the Bitcoin yield narrative explored later on, it is the most important narrative within MicroStrategy investment circles today. They form the basis from which an immense wealth transfer from new buyers to old ones is occurring. Let us start by investigating this premium to net asset value narrative, and the many shapes and forms it currently comes in.

Leveraged Play

With the growing amount of issued convertible debt for the purpose of accumulating more Bitcoin, investors found themselves warming to the notion that owning MicroStrategy shares instead of owning actual Bitcoin, was a “leveraged play” on the latter. Intuitively, it felt like the leverage was in strict proportion to the debt ratio. But Mark Meldrum rightly pointed out that this is misleading. If shareholders are levering by senior convertible debt, the leverage is rather to the downside than to the upside. If the share price increases, the debt is all converted into equity at conversion prices, diluting shareholders. If the share price decreases, the debt is not converted, but the shareholders must eventually pay the principal amount as well as coupons, if any.

Meldrum is slightly too harsh in his conclusion that there is no leverage to the upside. It should be remembered that the conversion prices of the various bond issues in general are about 35–50% above the price of MicroStrategy shares at the time of bond issuance. Because of this, there is leverage to the upside in proportion to the debt ratio of the company, but only up to the conversion price, at which the debt of the bond issue is eventually converted, and old shareholders must share in further price appreciation with the new ones. The upside from conversion price and onward has been given to the bond holders in the form of the free call options mentioned earlier, to make up for the low yield on the convertible bond issues. There was of course a valid reason MicroStrategy paid nothing in interest rate for some of its convertible bonds. The loans were not free. So with a conservative debt ratio of about 25%, the leverage quickly loses much power should the share price surpass conversion prices in a parallel move with Bitcoin. A large premium to net asset value can therefore not be explained by the company’s convertible bond issuance.

For investors seeking leverage on Bitcoin price movements, there is also an ever-increasing arsenal of instruments catering to that demand, such as levered Bitcoin ETFs as well as options with a Bitcoin ETF as underlying asset. None of these “levered bets” on Bitcoin carry the premium that MicroStrategy does. So paying more for a Bitcoin held by MicroStrategy, than for one you could hold yourself, must therefore not be excessively rationalized by pointing at “the leveraged play”. If anything, indirectly purchasing Bitcoin for a premium through MicroStrategy shares trading at high multiples to net asset value, means the investor is overpaying in proportion to the premium, for the doubtful privilege of getting leverage with equity features.

And finally, it is important to realize that past performance of the shares is not evidence of a “leveraged play” — it is only evidence of buyers bidding up the price. If the shares indeed have increased in price much more than Bitcoin — the company’s main underlying asset — it is simply because many investors believe that is how the stock “ought to behave”. If shares were to decline for a period of time while the price of Bitcoin goes up, that does not mean the company is some type of short play on Bitcoin. It would simply mean investors are selling shares for some reason, and others are buying Bitcoin for another reason. Causality hides in the fundamentals of company operations, not in the price discovery of jittery speculators. Looking at the slope of a Bitcoin per (diluted) share metric could give an investor a better picture of how large any “leveraged play” in practice really is, but the surest path is to dive into how the company capital structure actually functions.

Bitcoin Banking

Quant Bros, and others, also argued that the premium must persist due to the nature of the future awaiting a Bitcoin-laden MicroStrategy. Holding close to 2% of all existing Bitcoin by beginning of December 2024, it was now argued that the Bitcoin were to form the basis of the vague banking system of tomorrow, meaning any premium to net asset value must be due to various future banking activities with the Bitcoin as digital capital. There are multiple things wrong with this assumption.

First, MicroStrategy is a software company which has issued debt and equity to purchase Bitcoin. It is extremely generous to simply assume that they have an edge in banking, of all things. What is to say that other custodians such as Coinbase, Kraken, Binance or the likes, can’t offer better financial Bitcoin banking products and services? Or that more conventional banks such as Blackrock or JP Morgan ultimately won’t start accepting Bitcoin deposits? Banking is a sector which has painstakingly developed over many centuries, and to think that outsized profits related to it can be made by simply having accumulated a Bitcoin hoard is very naïve. Who will borrow the Bitcoin? For what purpose? What if there are large credit losses, private key incidents, or wrong choices in future chain splits? No such considerations are given when the Quant Bros are discussing, not a 2X premium, not a 3X premium, but a 60X premium to net asset value. Looking at Nvidia, not in the business of lending Bitcoin, but of producing extremely competitive microchips and related software, the comparison was still thought a valid one by the enthusiastic duo.

Curiously, Saylor also has a habit of comparing MicroStrategy to totally different companies:

“For people that haven’t been paying attention or don’t really do any research, if you actually logged into our earnings call or if anybody studied the company, that’s like saying there’s a perception that Microsoft trades are a premium to its underlying assets. Oh yeah, it does trades 50 times greater than its net tangible assets. So does Apple, so does Standard Oil, so does every operating company, so that the myth, the misunderstanding here is people don’t understand what our operating business is.” (x.com spaces, “Bitcoin as a National and Corporate Asset w/ Senator Lummis & Saylor”, 2024–11–19.)

What does it mean to MicroStrategy’s valuation, were it to actually become a proper Bitcoin bank? The average price-to-book ratio in the banking industry is slightly above one, as banks periodically mark-to-market assets and liabilities. Any multiple above one represents a premium stemming from expectations of future growth and excess earnings. Why a MicroStrategy morphing into an adventurous Bitcoin bank should fetch a high premium remained unexplained by the Quant Bros duo, which instead speculated that it didn’t “[…] think [MicroStrategy] being the most valuable company on the planet is widely unreasonable.” We have to remember that a premium for the company can’t be rationalized by pointing at general increases in the price of Bitcoin or in the past price action of the shares themselves — that is all irrelevant. A fund or an ETF trades at net asset value, regardless of whether the underlying asset goes up 100% or down 50%. So, a premium on MicroStrategy shares must come from investors expecting future growth, not in the price of Bitcoin, but rather in the Bitcoin per share metric. This expectation must also take into account the additional risk the company accepts in order to achieve this growth. Any conservative investor should not accept a valuation much higher than net assets, especially considering how the Bitcoin per share metric is engineered to increase, but more on that later. Many banks, while borrowing more cheaply than they lend out, trade at deep discounts to net assets due to the uncertainty of how solid the asset side of the balance sheet really is. As MicroStrategy ramps up convertible bond offerings, an outsized increase in a Bitcoin per share metric can very well be met with cracks spreading within its capital structure, should things take a turn for the worse in Bitcoin markets.

Saylor’s comparisons to Apple, Microsoft, Standard Oil and other companies trading at a premium to book value, are misleading mainly for the reason that those companies are not banks. Their assets are not liquid financial assets like MicroStrategy’s, and they may also have depreciated book values over decades to lower taxable profits, or simply booked assets a long time ago so that they no longer happen to reflect profits actually generated. Current cash flows from Windows software products likely far exceed whatever once was booked on the asset side of Microsoft’s balance sheet.

It should also be mentioned that most companies can’t very well issue shares and conduct arbitrage trades by simultaneously buying factories, office space, software or oil fields. MicroStrategy, however, can conduct arbitrage trades by issuing shares in order to buy Bitcoin, a liquid, fungible asset traded on hundreds of regulated exchanges, at all times of the day. The comparisons to fantastic price-to-book ratios in totally different industries are made to dazzle potential buyers of shares with back-of-the-napkin calculations on ridiculous net asset multiples. But none of it is real. Michael Saylor may speak of Bitcoin as digital energy, or of MicroStrategy as the crude oil refiner of futuristic finance — it is still wrong to assume that net asset valuations from that industry are at all relevant.

The Valuation Conundrum

There is no doubt that a lot of confident talk can be heard everywhere in MicroStrategy investor circles, with regards to the company’s premium to net assets. But talk is cheap as they say. Turning instead to the actions of the company and its leadership, greatly supported by investors, we will note that these actions fly in the face of the arguments the investors themselves simultaneously are making for any premium. MicroStrategy issues shares (equity), and convertible debt (equity if the share price goes up). This is, again, not a bad strategy while the shares trade at a premium to net assets. But it should be remembered that the company in this way slowly helps close the valuation gap that is the premium, by using the proceeds to purchase Bitcoin or pay off old debt. With a premium to net asset value close to three, at time of the commencement of the 21/21 Plan, the company could sell one Bitcoin worth of shares, and purchase about three Bitcoin on the open market, or redeem three Bitcoin worth of debt. This is an arbitrage by definition — Saylor labeled the 200% risk-free return as exactly that while on CNBC in December.

The glaringly obvious arbitrage explains why Saylor himself, as well as other company executives, have continuously sold shares throughout the year. It should be noted that Saylor’s selling plan was set in motion before Spring of 2024, when a considerable premium to net asset value had not yet materialized. Some investors argued that Saylor had to sell the shares, as previously received call options neared maturity date. But exercising the call options does not mean selling the shares is mandatory, unless there is some special clause we don’t know about. It just means the call options convert into shares at strike price. And even if it were the case that Saylor for one reason or another had to sell his newly received shares, the massive issuance and sale of company treasury shares would still have to be explained.

Some optimistic MicroStrategy investors were then quick to note that though Saylor’s selling was not mandatory, it was done to buy more Bitcoin personally. But if they believed it was in his interest to do so — in fact that it was “a genius financial move” — why did they fail to consider why it is not in their own interest to do the same? If Saylor considers the shares overvalued in terms of Bitcoin, perhaps due to the arbitrage he himself has mentioned on national television, why do investors who idolize his every financial move argue the exact opposite? On the whole it may be concluded that the company and its executives do exactly what some defenders of the premium deem “NAV multiple trading bullshit”, and there is a logical reason for that.

The constantly reoccurring SEC filings of executives selling company shares while never buying, do in fact hint of this truth which so few MicroStrategy investors dare think about. One wonders how many of these filings we must see before investors take note. Just after the announcement of the largest ATM offering in history, Senior Executive Vice President and Chief Financial Officer Andrew Kang sold 5,700 shares (Form 144, 2024–11–06). One day after, board member Leslie Rechan sold 20,000 shares (Form 144, 2024–11–07). The same day Senior Executive Vice President & General Counsel Wei-Ming Shao sold 20,000 shares as well (Form 144, 2024–11–07). Not a week later, Leslie Rechan cashed out on 20,000 shares yet again, netting about $5.5 million (Form 144, 2024–11–12). On the 13th of November, board member Stephen Graham sold 30,000 shares, netting over $11 million (Form 144, 2024–11–13). That very same day, Wei-Ming Shao sold another 18,000 shares, and the day after he sold more. CEO Phong Le sold shares on the 14th as well (Form 4, 2024–11–15). A week later, Stephen Graham sold a massive 20,000 shares further, netting $9 million (Form 144, 2024–11–21).

In the face of all this selling, investors still remained oblivious to the valuation conundrum the many narratives had obfuscated in their minds: Saylor, the other company executives, as well as the company treasury all appear to be massively selling the very shares that are supposed to be severely undervalued.

The Impossible Reboot

Seeing as company executives and the company treasury keep selling shares in ever larger numbers, consider for a second a situation where the premium is slowly captured in this manner, so that shares end up with a valuation closing in on that of actual Bitcoin holdings. In other words, where the net asset value multiple is nearing one. Is it suddenly impossible for Michael Saylor and MicroStrategy to pursue the banking adventure, which supposedly is a foundation to the premium in the first place? Of course not. The company can just as easily pursue its wild career starting with 500,000, 600,000 or 700,000 Bitcoin. There are no incentives whatsoever for the company to leave arbitrage on the table for others to try to capture, since Bitcoin banking does not depend on any premium persisting. It is rather amazing to watch MicroStrategy thought leaders viciously defend the premium while the company and its higher-ups are franticly devouring it.

Monopoly

There is another popular idea floating around in the MicroStrategy investing space, supporting the claim that the company should trade at a premium to net assets. It is the notion that “no one can catch MicroStrategy” in terms of the number of accumulated Bitcoin. The obvious question must then be, what this claim actually means, and why it should justify shares at a premium. If we are to assume that no other company will ever be able to own 2% of the total supply of all Bitcoin, that is all well and good, but what does that have to do with the premium? If owning such a large share of the supply somehow implies great profits in a future economy, it means the premium arises from being able to deploy the large Bitcoin stash for specific purposes. Why would not large Bitcoin custodians such as Coinbase, Kraken or Binance, perhaps sitting on even larger portions of Bitcoin, be able to apply their hoards in a similar fashion while sharing the profits with willing depositors? Would it be logical to say MicroStrategy “could never catch up”, because the company only sits on a few hundred thousand Bitcoin whereas some of these exchanges may have up to a million coins in custody? The notion is nonsense and has almost nothing to do with the fundamental value of MicroStrategy. Blinded by vast returns, many investors have stopped thinking when they assign a monopoly premium to the notion of simply owning more Bitcoin than others.

Additionally, it should be noted that smaller Bitcoin banks (or “treasury companies”) can compete with larger ones. Though consolidation occurs naturally in a free market, there have been many thousands of banks competing for customers over the centuries, some specializing in order to survive. The same would occur within a growing Bitcoin bank sector. There are no natural monopolies.

Regulatory Arbitrage

One prevalent argument in support of a sustained company premium to net assets concerns the so-called “regulatory arbitrage”. It is claimed that through innovative treasury operations, MicroStrategy can offer financial products to a regulated market which otherwise would have no opportunity to get exposure to Bitcoin. It should be remembered that MicroStrategy previously has discussed the premium in relation to the go-ahead of a Bitcoin ETF in January 2024. That day, shares fell sharply, only to quickly recover. Could it be that the premium to net asset value can be sustained due to the fact that, while many equity investors now have proper vehicles to get Bitcoin exposure, bond investors do not? The company’s convertible bonds have multiple times achieved large successes, so it has been logical to assume the regulatory arbitrage is real, and that MicroStrategy as sole issuer now could profit from it. But there are many things wrong with this assumption.

First, we must ask ourselves why there are all these huge funds that are allowed to own only bonds. The prevention does not stem from nowhere, but from self-regulation in the case of family offices, and from laws in the case of pension funds etc. These rules were put in place by someone for the specific purpose of minimizing risk, while still generating returns to clients. As bond owners, these funds stand first in line to company assets should bankruptcy threaten. Now, Bitcoin is a very volatile asset, and while it may seem obvious to some why potential returns from it can look tempting to bond portfolio managers, it is likely not obvious to those enforcing the risk management rules. Any loophole suddenly allowing for large exposure to a non-yielding digital asset which very few have expertise on, can be closed just as quickly as it was innovatively created. For this reason alone should it not be assumed that a “regulatory arbitrage” premium is large and long-lived.

How about other daredevils wanting Bitcoin exposure but can’t seem to find it due to regulations? Certain pension equity accounts may buy MicroStrategy shares, but not Bitcoin outright. Can a regulatory arbitrage premium persist through this type of investors? There is a case to be made here, but any premium would likely be very small, as agile investors could simply increase exposure to Bitcoin with their conventional savings, instead of paying a fee in proportion to the premium to net asset value when adding MicroStrategy to their pension accounts. It should not be assumed that people are not creative in finding the amount of Bitcoin exposure they are comfortable with, while minimizing more expensive, roundabout Bitcoin exposure through MicroStrategy.

So, we are mainly left with a, perhaps temporary, demand for bonds with Bitcoin exposure, before regulators swing their hammers. And while observing MicroStrategy history up to the 21/21 Plan but also after, we indeed see such actors willingly buying the bonds, even when conversion price is reflecting a huge premium to net assets. Has MicroStrategy actually found an alchemic formula here so strong, to start attracting trillions of dollars from the untapped bond market? The answer is likely no. The buyers of the bonds are likely not the type of family offices where an ”orange-pilled” heir has convinced the managers that “Bitcoin bonds” is the exposure needed to increase pitiful past performance.

No, what is likely happening with all the convertible bond issues is that MicroStrategy prices the bonds in a manner to attract market neutral hedge fonds, meaning arbitrageurs. Saylor has briefly mentioned these firms, as opposed to firms seeking actual Bitcoin exposure. For issue after issue, they can be spotted as the largest bond holders by anyone with a Bloomberg terminal. By buying the bonds, even when conversion price is at a large premium, and by simultaneously shorting the shares, these arbitrage funds can lock in close to risk-free profits. Due to the convex nature of the value of the convertible bonds, the hedge funds attempt to profit no matter whether MicroStrategy shares rise or decline: